A company’s financial performance is significantly influenced by its profit or loss accounts. Persistent financial losses can impact a company’s operational efficiency, limiting its growth prospects, and compelling a reconsideration of strategic objectives. This, in turn, may diminish its competitive edge, affecting its market position and shareholder relations. Moreover, companies must update investors and other stakeholders about any changes in their financial condition or operations that could affect the assessment of loss or its recovery. This could involve revising previous estimates, recognizing impairments, or disclosing new contingencies. The goal is to provide a complete and up-to-date view of the company’s financial health, including any factors that could potentially alter the risk profile of the business.

- Gains and losses are treated differently for tax purposes, depending on if they are short-term (usually occurring in 12 months or less) or long-term (taking place over more than one year).

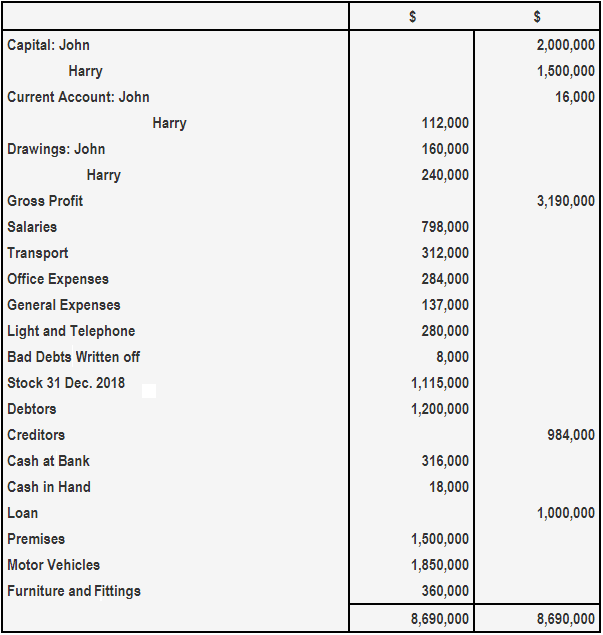

- When evaluating a profit and loss statement, it is important to consider statements from previous periods to get a more accurate sense of the rate of change in a company’s revenues and expenses.

- This is because the loss from a lawsuit is normally recorded based on an estimate when the loss is considered probable to happen.

- This is the money before the taxman takes his share, and it offers a clear picture of profitability from operations and secondary activities combined.

- A loss is an excess of expenses over revenues, either for a single business transaction or in reference to the sum of all transactions for an accounting period.

Presentation of a Profit and Loss Statement

The business incurs the expense when it completes each of the agreed rent periods. The law requires insurance companies to maintain an adequate reserve from which it will make payments of old claims, as well as the new claims anticipated in the next period. The standard level of reserves varies from 8% to 12% of the annual revenues, depending on the state laws.

Uncertainty and Financial Loss

Most companies report items such as revenues, gains, expenses, and losses on their income statements. Though some of the terms will sound similar, there are different practical uses for gains and losses, as well as for revenues and expenses. Extraordinary losses are those not incurred in the ordinary course of business and, generally, are infrequent and unusual. Thus, these are losses which a company would not expect to happen again in the foreseen future, or is highly unlikely to recur.

Our Services

Andy Smith is a Certified Financial Planner (CFP®), licensed realtor and educator with over 35 years of diverse financial management experience. He is an expert on personal finance, corporate finance and real estate and has assisted thousands of clients in meeting their financial goals over his career. Private companies, on the other hand, are not necessarily required to comply with GAAP. Some smaller companies, though, may not even prepare formal financial statements at all. The emphasis on liquid resources and cash flows, although useful for decision-making purposes, may not be relevant for income measurement purposes. Relative certainty and verifiability of measurements are satisfactory guides for income measurement purposes.

Gains are defined as increase in net assets other than from revenues or from changes in capital. To protect against unforeseen losses, companies typically invest in various insurance policies. For instance, a property insurance policy would cover losses from incidents like fire or flood. Some businesses taxpayer relief act of 1997 definition also acquire business interruption insurance to protect profits that would have been earned if a disastrous event occurs. Loss is the amount by which expenses exceed revenues within a given accounting period. It indicates that a company has spent more money than it has earned during that time frame.

Great! The Financial Professional Will Get Back To You Soon.

The transaction is recorded in accounts payable since it is a cost that the business needs to pay in the future. For example, if Company XYZ purchases goods worth $1,000 on credit, the company will have an incurred expense of $1,000. From gross profit margins to return on sales, these ratios paint a clear picture of financial health, allowing for comparisons across periods or even industries. By separating operational and non-operational revenues and expenses, it provides a more nuanced snapshot of a business’s health.

Examples can include losses from natural disasters, fires, or thefts that affect the business. The unique characteristic of these losses is that they are not connected to a company’s regular operational activities, and so, are considered separate from operating and capital losses. This classification allows investors and stakeholders to better judge a company’s normal operational performance. Loss is the excess of expenses over revenues for a specific period, indicating that a company has spent more than it has earned. It is reported on the income statement and negatively impacts the company’s financial health. Losses result from the sale of an asset (other than inventory) for less than the amount shown on the company’s books.

When this figure grows, businesses know they’re onto something; when it dwindles, it’s a clarion call to introspection. This team of experts helps Finance Strategists maintain the highest level of accuracy and professionalism possible. At Finance Strategists, we partner with financial experts to ensure the accuracy of our financial content.

Publicly traded companies are required to prepare P&L statements and must file their financial statements with the U.S. Securities and Exchange Commission (SEC) so that they can be scrutinized by investors, analysts, and regulators. Companies must comply with a set of rules and guidelines known as generally accepted accounting principles (GAAP) when they prepare these statements. Investors and analysts can use this information to assess the profitability of the company, often combining this information with insights from the other two financial statements. For instance, an investor might calculate a company’s return on equity (ROE) by comparing its net income (as shown on the P&L) to its level of shareholder equity (as shown on the balance sheet). Many common statistics, including t-tests, regression models, design of experiments, and much else, use least squares methods applied using linear regression theory, which is based on the quadratic loss function.